Last updated for 2026 Florida condominium reserve requirements.

Conceptual comparison of straight-line and pooled reserve funding methodologies. Detailed funding calculations and projections are presented within the reserve study report.

Florida condo boards commonly encounter this decision when preparing or updating a reserve study or Structural Integrity Reserve Study (SIRS).

Should our reserves be funded using a straight-line (component) method or a pooled (cash-flow) method?

This is no longer an academic distinction. The funding method selected affects annual assessments, long-term cash flow stability, statutory compliance, and how risk is distributed across future boards and owners.

This guide explains how each method works, how Florida law treats them, and how they are commonly applied in professional reserve studies prepared for Florida condominium associations in 2026. For boards that want a deeper technical explanation of each approach, we have also published detailed guides on straight-line reserve funding and pooled (cash-flow) reserve funding, which expand on the calculations, assumptions, and real-world implications of each method.

Quick Navigation

- Understanding the Two Reserve Funding Methods

- Component Method (Straight-Line Funding)

- Cash Flow Method (Pooled Funding)

- Side-by-Side Comparison

- Application to SIRS Components

- What Florida Law Actually Requires

- Best Practices for Florida Condo Boards

- Final Takeaway

Understanding the Two Reserve Funding Methods

Professional reserve studies in Florida generally model funding using one of two approaches:

- Component Method, commonly referred to as straight-line funding

- Cash Flow Method, commonly referred to as pooled funding

The correct choice depends on the association’s building complexity, risk tolerance, funding philosophy, and compliance obligations. Neither method is inherently “better”; however, each produces materially different outcomes over time.

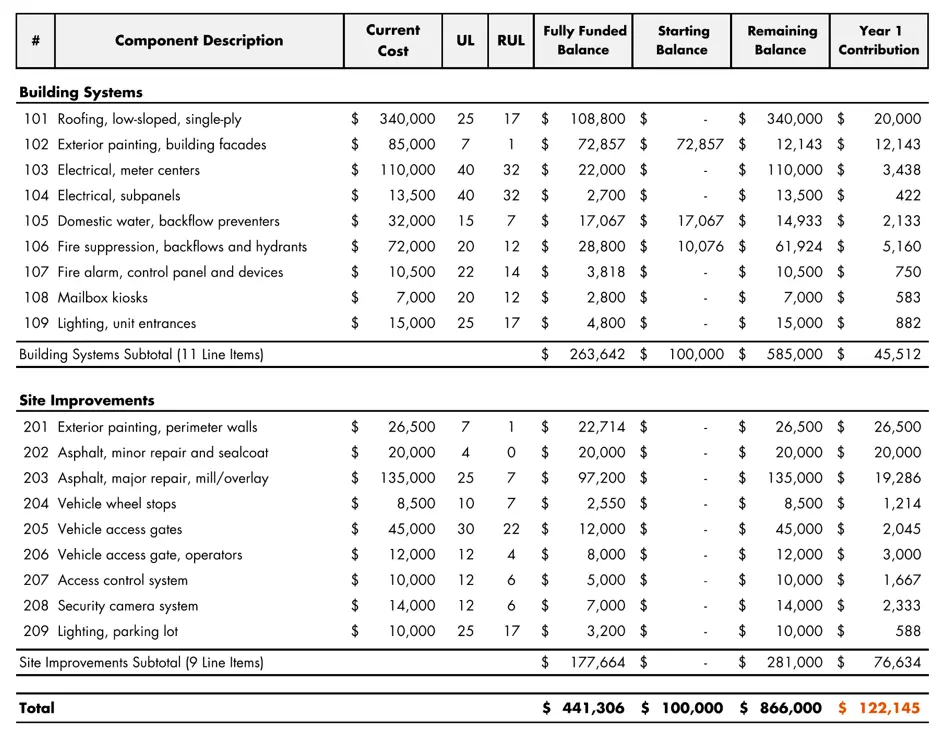

Component Method (Straight-Line Funding)

The component method calculates reserve contributions independently for each reserve item. Each component’s remaining cost is divided by its remaining useful life to determine the annual contribution.

How it works in practice:

- Each reserve component stands alone

- Contributions are recalculated periodically

- Inflation and investment income are not directly considered

Typical characteristics:

- Highly transparent at the individual component level

- Conservative by design

Common limitations observed in practice:

- Limited flexibility when repair timing shifts

- Can lead to higher near-term contributions

- Does not optimize cash flow across components

Example report excerpt:

For a more detailed explanation of how straight-line funding is calculated, including component-level assumptions and limitations, see our in-depth guide on straight-line reserve funding.

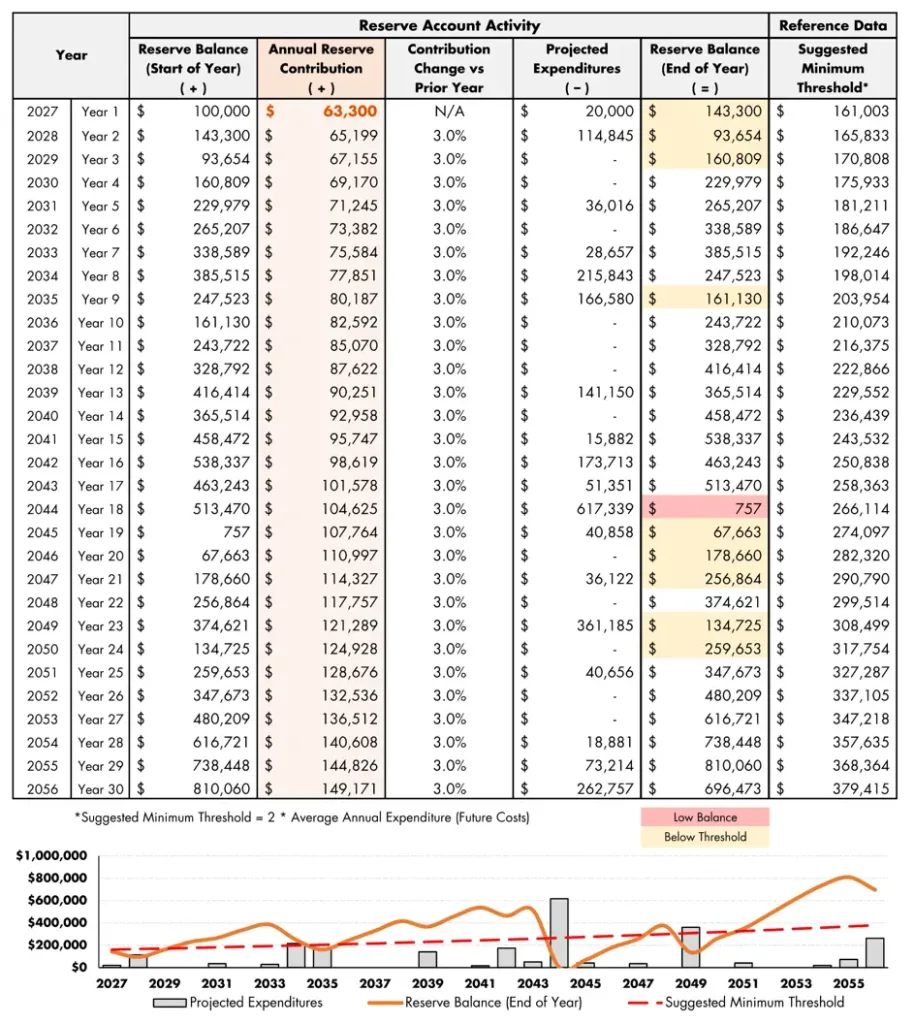

Cash Flow Method (Pooled Funding)

The cash flow method evaluates the reserve account as a whole over a multi-year projection period. Contributions are structured to keep the reserve balance above a defined minimum threshold while accounting for inflation and interest earnings.

How it works in practice:

- All applicable components are pooled within a reserve category

- Annual contributions may vary year-to-year

- Inflation and investment income are explicitly modeled

Common funding goals include:

- Baseline funding: balance remains positive but may approach zero

- Threshold funding: balance remains above a board-defined minimum

- Full funding: balance tracks close to the fully funded balance

Observed advantages:

- Improved long-term cash flow efficiency

- Better alignment with real-world repair timing

- Reduced likelihood of unnecessary overfunding

Example report excerpt:

For a deeper discussion of cash-flow modeling, funding thresholds, and contribution smoothing, see our in-depth guide on pooled reserve funding.

Side-by-Side Comparison

| Category | Component Method (Straight-Line) | Cash Flow Method (Pooled) |

|---|---|---|

| Primary focus | Individual components | Overall reserve balance |

| Contribution stability | Fixed year-to-year | Variable year-to-year |

| Inflation modeled | No | Yes |

| Investment income | No | Yes |

| Flexibility | Low | High |

| Best suited for | Smaller or simple communities | Larger or complex communities |

The table below summarizes the practical differences boards experience when selecting a reserve funding methodology.

Application to SIRS Components

Florida law requires that SIRS-mandated components be fully funded and separately identified, but it does not prescribe a specific funding methodology.

In practice, this means:

- SIRS components may be funded using straight-line or pooled methods

- SIRS components must be segregated from non-SIRS reserves

- The reserve balance may not fall below zero

- The funding method must be clearly disclosed

Example disclosure language:

“SIRS-required components are presented as a separate reserve category and funded using a pooled cash-flow methodology to ensure statutory compliance while maintaining long-term contribution stability.”

Visit our in-depth guide to the Structural Integrity Reserve Study (SIRS) for more information.

What Florida Law Actually Requires

Florida Statute §718.112(2)(g) establishes what must be funded, not how it must be funded.

Key points boards often misunderstand:

- A unit owner vote is not required to change funding methods

- Pooled funding remains legally permissible

- Straight-line funding is not mandated for SIRS

Boards retain discretion, provided the reserve study and budget clearly document the methodology used.

Best Practices for Florida Condo Boards

- Use a professionally prepared reserve study, not spreadsheet assumptions

- Clearly separate SIRS and non-SIRS reserve categories

- Select a funding goal aligned with risk tolerance and assessment stability

- Reevaluate funding assumptions after inspections, major repairs, or material cost changes

Final Takeaway

The correct reserve funding method is not a matter of preference or tradition. It is a financial planning decision with long-term consequences.

What matters most is that your reserve plan:

- Complies with Florida statute

- Fully funds SIRS-required components

- Matches your community’s risk profile and planning horizon

- Is clearly documented and defensible

Straight-line funding prioritizes simplicity and conservatism. Pooled funding prioritizes flexibility and cash flow efficiency. Both can be compliant when applied correctly.

If your board is reassessing its funding approach or transitioning under the post-2025 regulatory environment, professional guidance matters.

Questions about which method is appropriate for your association?

Contact Criterium-Cromer Engineers to discuss your specific building, funding history, and compliance obligations.